Companies should no longer be allowed to deny mortgage or insurance services to cancer survivors without explanation or a transparent risk assessment, say patient advocates. A few hopeful signs show their message may be getting across.

It was in November 2010 that Nicky, a young government worker in Belgium, was diagnosed with lymphoma. It was treated by radiotherapy, and by the start of the New Year in 2011 the therapy was over and the cancer was gone.

“I was only 23 and I tried to move on – but two years later, in June 2013, my boyfriend and I decided to start building a house. We went to the bank and got a loan to finance our building project. Next, we applied to convert my life insurance, which I had taken out before my cancer, to pay off my share of the house loan if necessary. To do this I had to fill in a form with questions about my medical background – but my boyfriend’s insurance was accepted and I got a rejection letter.

“I was stunned. I had expected that they would charge extra or that they would put some exceptions in the conditions. I thought that they had made a mistake or did not understand the type of cancer that I had suffered. So I asked for an explanation.”

I thought that they had made a mistake or did not understand the type of cancer that I had suffered.

All Nicky received was one sentence stating the disease and treatment and that she was still in ‘follow-up’ – there was nothing about why she was too big a risk. “I have been trying so hard to learn to live with what happened to me and then an insurance company says they expect that I will die in the next 20 years? It may not be what they said, but it sure is what it feels like. By not granting me insurance they made me feel different – all I have been trying to do since my cancer is to feel normal again.”

This is said to be an all too common problem for cancer survivors around Europe. Not only do people have to contend with the denial of insurance that can be vital to carrying on with daily life, but the reasons are often not communicated. In just one sentence, a life or travel insurance company can stop someone from enjoying the security or holiday opportunities that other people take for granted.

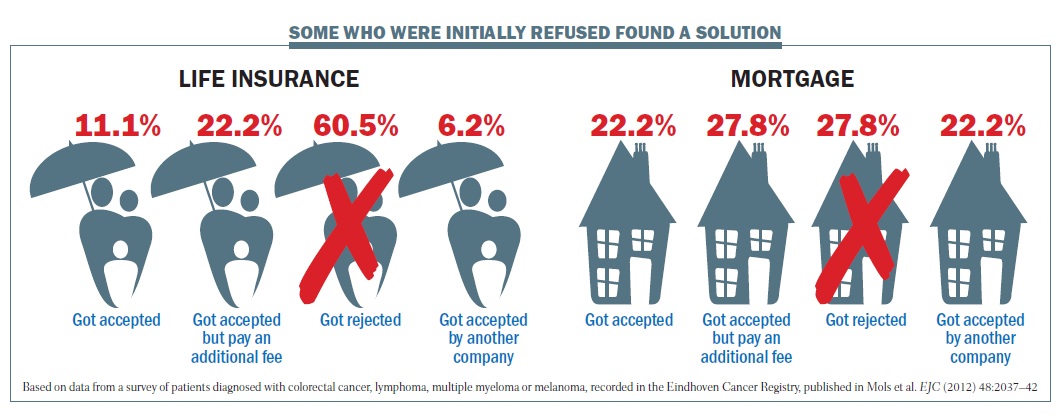

More research is needed on just how many are affected, but a recent study in the Netherlands found that life insurance is a particular problem for cancer patients, with a fifth having problems, and of these, more than 60% were rejected (Mols et al. EJC 2012 48: 2037–42). Further, cancer patients often encounter other financial difficulties, especially related to employment if they are unable to work at the same level owing to long-term effects.

Asking the company to review her case, Nicky finally got some figures that her own doctor said were incorrect, and asked for advice from the Flemish League against Cancer. So far, however, she has been unable to change the company’s position. She does have other options – for example to try for insurance elsewhere, risking further rejection, and appealing to Belgium’s Interfederal Centre for Equal Opportunities, which she has now done.

A widespread problem

Ward Rommel, a researcher at the Flemish League Against Cancer, says that insurance is one of the main financial issues facing cancer survivors, particularly the younger ones. “Often they still have to buy a house, start a business or have yet to take out life insurance – so for them it’s a real problem. Young men who have had testicular cancer, or those with Hodgkin’s lymphoma, are among those more commonly affected.” When people are able to obtain insurance it is often only with a high premium, he adds. It is important to note that most European countries do have good public insurance programmes for welfare and health, although those relying on extra private health insurance that is outside of government mandates will often run into exclusions for cancer. Even the US has recently ruled out discriminating against preexisting conditions in obtaining private healthcare insurance in its recent (and controversial) ‘Obamacare’ reform. “It is the market for other types of private product that is the main problem, such as covering a mortgage with life insurance,” says Rommel. “As well as difficulties that cancer patients face in obtaining insurance, they often also complain about the lack of transparency about decisions [as in Nicky’s case], and it can be difficult to get information from an insurance company’s doctor.”

Belgium, in common with many European countries, has an ombudsman for the financial services industry, which adjudicates in disputes between customers and companies. However, it can take considerable time for an ombudsman to reach a decision, especially in more complex cases, which are common in cancer.

The UK’s ombudsman takes a minimum of several months for basic cases and it could be a year or more for complex cases, which can be reviewed and appealed several times. All decisions are published on their website. As an example of complexity, one judgement on a refusal to pay out on a critical illness policy for prostate cancer hinged on whether medical evidence indicated that the Gleason score and TNM classification of the complainant’s tumour was below the insurer’s exclusion criteria (the ombudsman eventually found against the complainant). A payment could depend on whether a cancer is deemed invasive or not – with all that entails in medical judgement.

But there are many complaints that have been upheld about insurance terms being hidden in ‘small print’, and also being blatantly missold: in the UK there has been a major scandal about mis-sold payment protection policies, resulting in refunds of more than £15 billion. But the position taken by regulators and ombudsmen is that insurers are entitled to sell policies with terms and exclusions they want (although not for illegal reasons such as race), as long as customers are always alerted to the terms and what they mean.

Could insurers do more?

Could insurers do more?

The bigger question is whether insurers could do more for people with pre-existing conditions and those who develop serious illness, as well as being fair and transparent with existing policies. Rommel, who is leading on financial services work for the Association of European Cancer Leagues (ECL), says there has been some attention at European level – notably in 2011 at a survivorship conference at the European Parliament – and a major report, ‘Current practices of financial services providers’, was prepared by Civic Consulting in 2010 for the European Commission. The report notes that better competition between insurers can serve low-risk people well, as companies target them with lower- priced products, but high-risk consumers could be priced out of the market or refused insurance.

Insurers put their point of view forward at a recent survivorship summit run by Europe’s main cancer trials group EORTC (see also Cancer World May–June 2014). John Turner, an underwriter from reinsurer Swiss Re, pointed out that more than €600 million is paid out each year by the European life insurance industry, and cancer is the leading cause, ahead of cardiovascular causes. This is because cancer is more likely to be a disease among the insured and also because insurers are less accurate at predicting risk for cancer than they are for heart problems. “We have few scoring tools for cancer: one is smoking and the other is have you already had cancer, so for survivors that is the single biggest predictor of mortality we have for the risk selection process.”

Turner argues that the industry has no incentive to spend a lot on risk analysis if they are only going to decline people. “But the problem we have is: how do we make it insurable? It is still a serious threat to life. If we don’t have the premiums that match the risk, we will go out of business.” He says the industry is busy feeding in the latest survival data into its calculations, but given how many people die in the first few years after diagnosis, it is unfeasible to take on that risk in many cases. There is a time point, however, depending on the type and stage of cancer, at which people become insurable, at least initially for a higher premium, although a normal premium may be offered when there is a certain duration since diagnosis and for milder forms of cancer.

As an example of rapid progress, he said, a woman diagnosed with stage 1 ER-positive breast cancer is actually insurable the next day – whereas she wasn’t in 1995, although she would pay an extra €5 per €1000 insured for three years, which could amount to a lot if the sum insured is large. “But what does the risk mean – because that’s the key area where we have miscommunication between the treating physicians and the physicians working for insurers. That ‘five per mille’ represents a half a per cent of those patients dying – most doctors treating a patient would say that is a low risk. But from an insurance perspective that number is huge because it is a large multiple of the standard risk, which we have to take into account otherwise the whole structure of voluntary insurance falls down.”

Overall, Turner said, one of the insurance industry’s biggest problems is that for long-term products such as life insurance – which could last 25 years or more – it is hard to set prices based on evidence that will get outdated as fiveyear survival rates improve, such as in breast cancer. But with cancers such as Hodgkins, for instance, where survivors are almost five times as likely to develop a second cancer in the next ten years compared with the general population – and with cancer causing such a large proportion of claims in critical illness and life insurance – insurers cannot afford to ignore the risk.

With the many hundreds of companies around Europe offering insurance, it is not surprising that many may not have the resources to keep on top of the complexities, and operate instead on broad principles that can often result in blunt denials or massive surcharges. Even specialist providers, such as those that insure travel for cancer patients, say they need much more data, as the EORTC summit heard.

Even specialist providers, such as those that insure travel for cancer patients, say they need much more data

A case for regulation?

Naturally, insurers are not supportive of more regulation, but a voluntary system that brings parties together could help more patients obtain insurance, by say explaining a denial and offering more evaluation on the medical position. France has taken a lead, says Rommel, with the AERAS convention (s’Assurer et Emprunter avec un Risque Aggravé de Santé, or ‘insuring and borrowing with a higher health risk’), an agreement between the financial services industry, patient groups and government. It allows for speedy acknowledgement of medical progress, several evaluation levels for people denied insurance and capping of high surcharges.

Now Belgium is adding more teeth to this type of arrangement by implementing a law that, from January 2015, should improve access to home loan insurance for people with a higher health risk. The law was first enacted in 2010 but is only being implemented now that opposition from insurers has been overcome.

People in the UK are covered by broader legislation. The country’s Equality Act has rules about insurance for people with disabilities (“disability” being a catch-all term that includes illness) that mean companies must use reliable medical information and not refuse to cover cancers that can be well-managed or are curable, but it does not have a special initiative like AERAS or the new Belgian law.

Meanwhile, the EU may extend its equal treatment directive, which could give similar protection to people across Europe. The intention is to tackle discrimination on access to services and goods not already covered by existing European law (such as on gender discrimination), by extending the directive to cover age, sexual orientation, religion and disability. This should help ensure that people with long-term health conditions get more favourable responses from the insurance sector. But it has been stalled for six years due to opposition, notably from Germany. “ECL has been among those lobbying for it, but hopes for progress now lie in the new European Parliament,” says Rommel.

Extending the EU equal treatment directive could improve access to insurance for people with health conditions

Cancer advocates will certainly continue to argue for better services for survivors and patients. In February, a new bill of rights for European cancer patients was launched by the European Cancer Concord, run by the Society of Translational Oncology, but it focuses mainly on care issues and makes no mention of problems such as financial matters. Rommel feels this is an omission and points to a local patients’ bill of rights in Flanders, put forward by the Flemish League Against Cancer, where access to insurance is mentioned, and ECL issued similar guidelines for cancer patients’ rights in 2004. “A stronger call for broader rights is lacking at European level and we should address this,” he concludes.

Leave a Reply